The City of Chicago just put real money on the table for homebuyers — up to $70,000 of it. The new HomeGrown Purchase Assistance Program, announced by Mayor Brandon Johnson and the Chicago Department of Housing, will hand eligible buyers a grant toward their down payment and closing costs starting Monday, June 8. I've spent 30+ years helping people buy homes in this city, and I can tell you that a grant of this size — money you don't pay back — is the kind of thing that turns "someday" into "this year" for a lot of working families. But the details matter, the funding is limited, and the buyers who understand the rules first will be the ones who actually get the check. Here's everything you need to know.

What the HomeGrown Program Actually Is

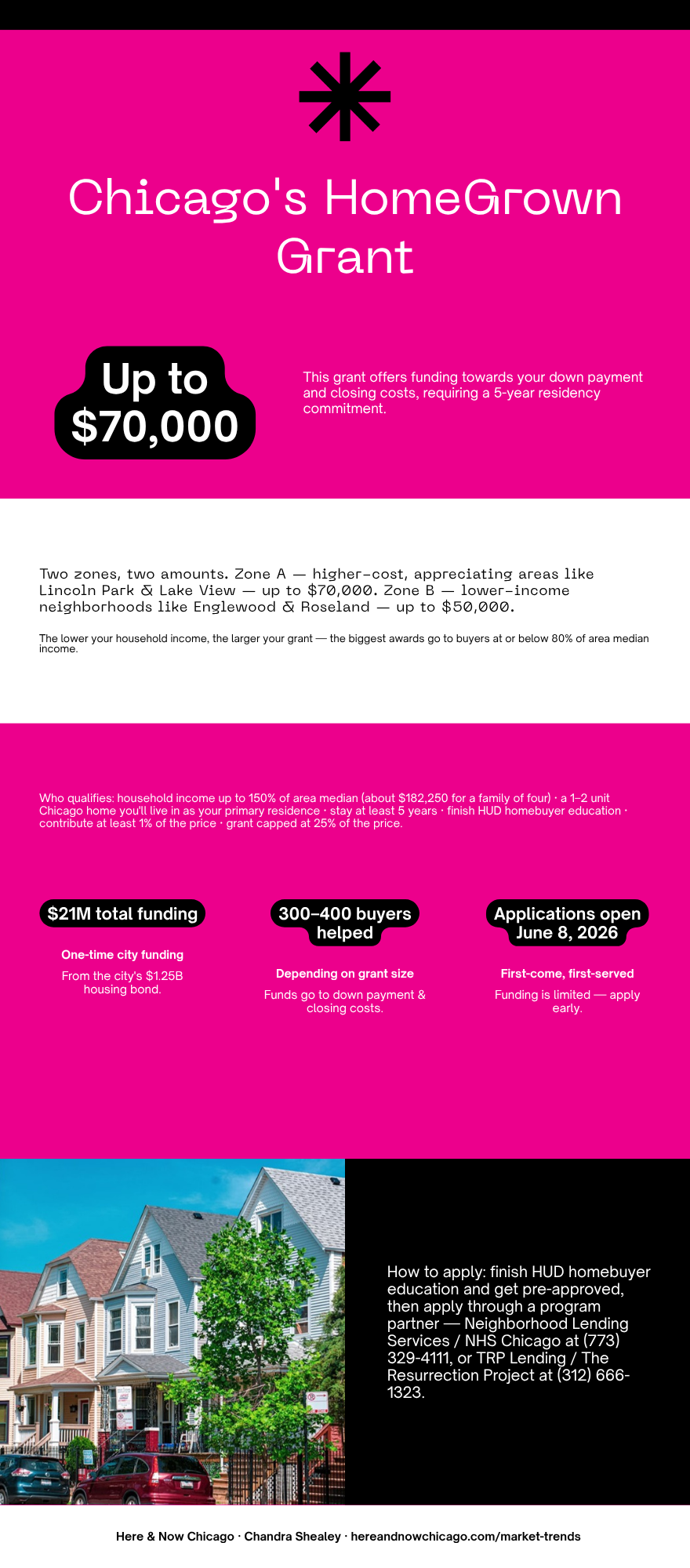

HomeGrown is a $21 million down payment and closing-cost assistance program, funded out of Mayor Johnson's $1.25 billion Housing and Economic Development Bond. The city expects it to help 300 to 400 buyers, depending on the size of each grant awarded. Applications open June 8, 2026.

The headline number is up to $70,000 — but that top figure isn't a flat amount everyone receives. The grant is tiered, and how much you can get depends on two things: where you're buying and what you earn (more on both below). The money can go toward your down payment and closing costs, which are the two cash hurdles that keep most would-be buyers renting longer than they'd like.

This is structured as a grant, not a loan you repay month to month — but it does come with a commitment to stay in the home (I'll get to that). The program is administered by two well-respected local nonprofits selected through a formal city proposal process: Neighborhood Lending Services, an affiliate of NHS Chicago, and TRP Lending, an affiliate of The Resurrection Project. These aren't fly-by-night operators — they've been doing affordable lending and homebuyer counseling in Chicago neighborhoods for decades.

One honest caveat worth stating up front: the city has described this as a one-time funding effort, with the possibility of revisiting it if it succeeds. Translation — don't treat this as a program that'll be sitting around next year. Treat it as a window.

As Destiny Durham, the Department of Housing's homebuyer programs project manager, put it: "We don't want to continue to have homeownership be out of reach for many working families." That's the whole point of this thing.

How Much You Can Get — and Why Your Neighborhood Decides

This is the part that surprises people, and it's the part where having an agent who reads the fine print actually pays off. HomeGrown divides the city into two zones, and the zone your home sits in sets your maximum grant.

Zone A — up to $70,000. These are areas where home prices have climbed significantly — neighborhoods like Lincoln Park and Lake View. The logic is straightforward: it costs more to buy into an appreciating neighborhood, so the assistance is larger to help working families compete there rather than get priced out entirely.

Zone B — up to $50,000. These are lower-income census tracts — areas where 70% or more of families earn below 80% of the statewide median family income. Neighborhoods like Englewood and Roseland fall here. The assistance is still substantial; it's calibrated to the lower price points in these communities.

On top of the zone, the grant scales with your income — the lower your household income, the more help you're eligible for. The largest awards go to buyers at or below 80% of the area median income. So the full $70,000 isn't a number most buyers will hit; it's the ceiling for a lower-income household purchasing in a high-cost Zone A neighborhood.

The city has set up a program website where you can look up a specific address and see which zone it falls in. My advice — and this is exactly the kind of thing I do with clients — is to figure out your zone before you fall in love with a house, not after. Two homes a few blocks apart can sit in different zones, and that difference can be tens of thousands of dollars in assistance.

Who Qualifies

HomeGrown has a clear set of requirements. You'll need to satisfy all of them, not just some:

Income. The income cap depends on your zone, so check yours before you assume you qualify. In Zone A, your household's gross annual income can't exceed 120% of the area median income; in Zone B, the ceiling is higher at 150% of AMI — which works out to roughly $182,250 for a family of four, or about $127,650 for a single buyer. (Exact dollar limits vary by household size and zone — the official income chart is posted at chicago.gov/homegrown.) It's a wide net, but the Zone A and Zone B ceilings are different — a buyer who'd clear the bar in Zone B can be over the limit a few blocks away in Zone A. This is exactly why your zone matters.

Homebuyer education. You must complete a HUD-certified homebuyer education course. This isn't busywork — it's a genuinely useful walk through budgeting, credit, and the mechanics of closing. Both administering nonprofits offer it, and the certificate is a required document in your application.

The property. You have to buy a home in Chicago that you'll live in as your primary residence. Eligible property types are single-family homes, condos, townhomes, and two-unit properties — buildings with three or more units don't qualify. The program applies to existing homes citywide — it's not limited to new construction. That two-unit allowance is a quiet gift, by the way: buy a two-flat, live in one unit, rent the other, and you've got a tenant helping cover your mortgage.

Occupancy. You must commit to living in the home for at least five years as your primary residence.

Your own skin in the game. You're required to contribute at least 1% of the purchase price from your own funds. On a $350,000 home, that's $3,500 — a modest, reasonable ask that ensures buyers have some personal investment.

The grant cap. Assistance can't exceed 25% of the purchase price before any other purchase help is applied. So the grant is meant to close a real gap, not to fund the entire down payment on a low-priced home.

The Fine Print Worth Understanding

I'd be doing you a disservice if I only sold you the upside. A few things deserve a clear-eyed read.

The five-year occupancy commitment is the real string attached. This is money toward a home you intend to live in and keep — not a flip, and not a rental you move out of in year two. The grant is forgiven gradually over those five years — roughly 1/60th a month — so if you stay the full term, it's money you don't repay. But if you move out, sell, or take cash out of the home before the five years are up, the unforgiven balance has to be paid back to the city. If staying put for five years sounds fine, this is about as close to free money as it gets. If you're not sure where you'll be in three years, think hard before you commit.

The 25% cap and the "before other assistance" language matter when you start stacking programs. HomeGrown is designed to combine with other help, but the cap is measured against the purchase price first. A good lender and your program counselor will run the actual math for your situation — don't eyeball it.

And the big one: funding is limited and awarded first-come, first-served. Twenty-one million dollars sounds like a lot, but spread across grants this size, it covers only 300 to 400 households. When this kind of assistance launches in Chicago, the early applicants are the ones who get funded. The buyers who close are the ones who showed up to June 8 already pre-approved, already counseled, already clear on their zone.

How HomeGrown Fits With Other Programs

HomeGrown doesn't exist in a vacuum, and one of the most common questions I'll get on this is "Can I combine it with everything else?" The short answer is that down payment assistance is meant to be layered intelligently — within that 25% cap.

It's worth knowing the broader landscape. The Illinois Housing Development Authority runs several first-time-buyer programs — forgivable and deferred down payment assistance in the $6,000 to $10,000 range. Conventional loans go as low as 3% down for first-time buyers, and FHA loans as low as 3.5% with more forgiving credit requirements. Eligible veterans can use VA loans with nothing down. I broke all of these down in my first-time buyer's guide to Chicago, and the playbook there still applies — HomeGrown just adds a much bigger lever to it.

The right combination depends entirely on your income, your credit, your zone, and the home you're buying. This is where a lender who actually knows these programs earns their keep. My preferred lenders work with city and state assistance programs every week and can tell you in one conversation how the pieces fit together for you specifically.

How to Apply

The application runs through the two administering nonprofits, and the process is a clean six steps: confirm you meet the income and residency requirements, verify your property's zone, gather your documents, submit your application, go through eligibility review, and coordinate the funds with your purchase.

The document list is standard but specific. Have these ready:

- Identification — government-issued ID (ITIN documentation if applicable)

- Income — three recent paystubs (last 30 days) for every household member 18 and older, two years of federal tax returns with schedules, and two years of W-2s or year-end Social Security/pension statements

- Purchase paperwork — a signed purchase contract, your mortgage pre-approval, and your loan estimate if you have it

- Your homebuyer education certificate

You can apply through either administrator:

Neighborhood Lending Services / NHS Chicago — (773) 329-4111, homeownership@nhschicago.org — nhschicago.org

TRP Lending / The Resurrection Project — (312) 666-1323, 1818 S. Paulina St., Chicago, IL 60608 — resurrectionproject.org/homegrown. The Resurrection Project offers services in Spanish, which matters for a lot of Chicago families.

You can also start at the city's official program page at chicago.gov/homegrown to look up your zone and confirm the current details before you apply.

If it helps to see it all in one place, I put the whole program on a single page — the HomeGrown grant at a glance — with the two zones, who qualifies, the dollar amounts, and the dates that matter. Save it, or send it to someone who's been waiting for a reason to start.

{kind=link}

My strongest piece of advice: don't wait until June 8 to start. Knock out your homebuyer education course now. Get a real pre-approval — not a pre-qualification — from a lender who understands assistance programs. Identify the zone of the homes you're considering. Do that prep work this week, and on launch day you're submitting a complete application while other buyers are just beginning to read the requirements.

What This Means for Chicago Buyers

Here's my honest read after three decades in this market: programs like HomeGrown don't come around often, and when they do, the money moves fast. A $70,000 grant doesn't just shrink your down payment — it can be the difference between buying in the neighborhood you actually want and settling for the one you can barely afford. It changes which front doors are open to you.

But a grant is only useful if you're positioned to act on it. The buyers who win in a first-come, first-served program are organized, pre-approved, and clear-eyed about their numbers before the application window opens. That's exactly the part I help with — figuring out your zone, matching you with a lender who knows how to stack HomeGrown with other assistance, and getting you to a contract while the funding is still there.

If you've been wondering whether homeownership in Chicago is within reach this year, the answer may have just changed. Let's talk about where you want to live and what you qualify for — start with our Buying Power Calculator, and then reach out. No pressure, no obligation. Just real guidance on how to put this program to work for you before the window closes.